Five for Friday – July 10, 2026

Momentum, Shock Absorption, Jobs, Where Time Goes and Satellites

1. Mo'

Despite an action-packed start to 2026 that included war in Iran, the longest government shutdown in history, and volatile market action, the S&P 500 closed out the first half of the year up 10.2% and within a hair’s breadth of its all-time high. And while the market’s ongoing AI enthusiasm continues to fuel bubble worries, first-half strength has been a positive harbinger more often than not. Over the last century, for the 39 years in which large-cap stocks were up 10%+ in the first half, the second halves had a median return of 11% (with a positive return in 32 of those 39 years). The first-half move in small-cap stocks was even more potent (+21% for the small-cap Russell 2000 index), and has historically portended second-half outperformance as well. Just like in physics, a body in motion tends to stay in motion. That may not always be a positive thing, but for today the bull market continues and history hints at a solid second half.

2. Shock

With the Strait of Hormuz back in focus, it’s worth considering the broader impact of major disruptions to oil supply wrought by a single chokepoint. Shocks to a system are painful but they also expose vulnerabilities and force adaptation. The 1970s oil crises led to the creation of the Strategic Petroleum Reserve and catalyzed non-OPEC production. Covid-era supply-chain disruptions pushed companies to diversify suppliers and build redundancy, and so on. The same logic applies for resilience being built today. Energy markets now appreciate more fully the risks of heavy dependence on the Strait of Hormuz, and incentives exist to reduce that dependence. Baird Senior Research Analyst Mig Dobre estimates that the UAE alone could invest over $30 billion in Hormuz-bypassing infrastructure in coming years (see: West-East 1). Qatar and Kuwait are likely to pursue similar projects and Saudi Arabia is looking to expand pipeline capacity to the Red Sea. Shocks create pain, capitalism creates a profit motive to cure that pain, and competition fuels innovation. Whether the challenge is compute or crude, that’s the system working.

3. Jobs

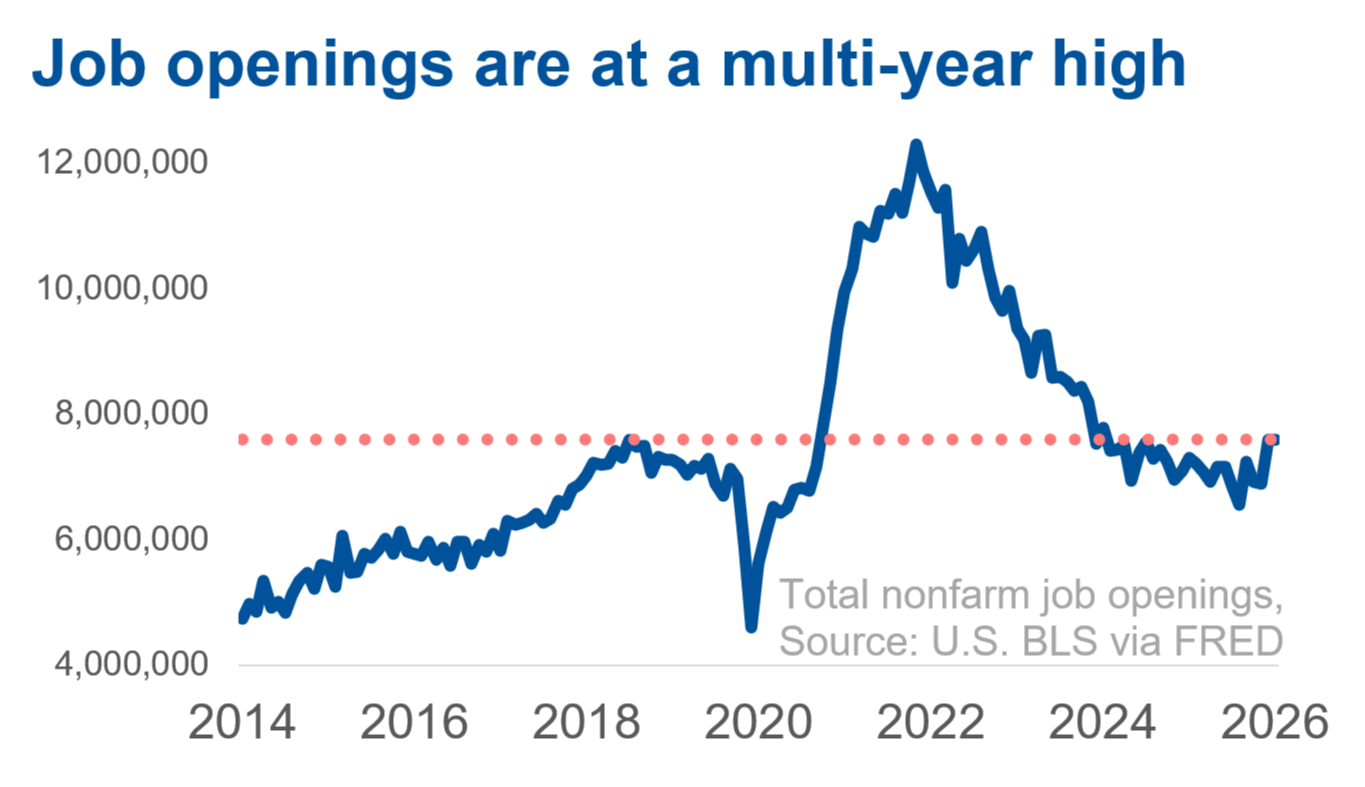

The labor market backdrop is far from perfect, but there are green shoots to celebrate. The first half of 2026 featured the best rate of payroll growth in cyclical industries (a category that excludes government, healthcare, and education) since 2023 and the unemployment rate sits at a 12-month low. Perhaps more critically, job openings seem to have bottomed and now sit at their highest level since early 2024. This goes hand in hand with a growing bank of research suggesting is AI not only not fueling mass job loss, but may even be creating demand for workers. Things can change quickly, but for now the labor market is striking an investor-friendly balance: strong enough to keep consumers spending, but not so robust as to demand interest rate hikes.

4. Time

Last month, the BLS released its American Time Use Survey, a national analysis of how Americans allocate their most finite resource (and a unique and interesting dataset for investors). Because it measures how Americans actually spend their time, it can provide an alternative look at shifts in consumer behavior and labor-market trends. On the rise: video games, food prep and cleanup, and time with pets. On the decline: socializing, reading, and work-related activities.

5. On This Day

in 1962, the world's first active communications satellite – the Telstar 1 – was launched into orbit, quickly proving its value by relaying broadcasts, phone calls, and data across the Atlantic and laying the foundation for today’s global communications network. While the Telstar 1’s life was short, the mission established the feasibility of connecting distant regions through orbiting infrastructure, an idea front-and-center today with SpaceX’s IPO and the satellite boom.

Disclosures

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Market and economic statistics, unless otherwise cited, are from data provider FactSet.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should not consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For investment advice specific to your situation, or for additional information, please contact your Baird Financial Advisor and/or your tax or legal advisor.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Copyright 2026 Robert W. Baird & Co. Incorporated.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.